It started, as it always does, with an email.

The file was a standard residential closing. The processor, Lisa, was on her twelfth file of the week. The seller, a remote property investor, had been communicative and professional. All the documents were in, the title was clear, and the closing was scheduled for Friday.

On Thursday afternoon, an email landed in Lisa's inbox.

Subject: Updated Wiring Instructions - [File #12-884B]

The email looked perfect. It used the seller's correct name, the file number, and a familiar, slightly urgent tone. It explained that due to an issue with their primary bank, the seller needed the proceeds sent to a different account. The new instructions were in the attached PDF.

Lisa replied to the email to confirm the change. The fraudster, posing as the seller, replied immediately: "Yes, confirmed. Thanks for checking."

The next morning, Lisa wired $240,000.

A couple hours later the real seller called asking where his money was. By then, it was gone forever. This is a post-mortem of the exact moments the title company's process failed, allowing a simple email to become a catastrophic, unrecoverable loss.

The Failure Points:

A Moment-by-Moment Analysis

The $240,000 wasn't lost in a single moment. It was lost in a chain reaction of two small, seemingly innocent process gaps that exist in thousands of title companies today.

Failure Point #1: The Inbox as the Source of Truth

The entire fraud was initiated and executed within the email inbox. The processor received a critical financial directive through the most insecure communication channel possible. The company's workflow treated an email attachment as a legitimate, actionable document.

- The Gap: The process relied on a human employee's ability to spot a sophisticated fake in a busy inbox. The fraudulent email used a spoofed domain that looked nearly identical to the real one, a tactic that bypasses most spam filters.

Never use email to communicate wiring instructions.

Failure Point #2: The Flawed Verification Protocol

The company had a policy: "Verbally confirm all wire instruction changes." The processor believed she was following this rule by replying to the email. This is the most common mistake in verification. "Verbal confirmation" is useless if you are talking to the criminal.

- The Gap: The policy did not mandate out-of-band verification. It did not require the processor to disregard all contact information in the new email and use only the original, verified phone number from the opening package.

The Aftermath:

Beyond the Financial Loss

The $240,000 was just the beginning. The aftermath involved a frantic call to the FBI, a notification to the company's E&O insurance carrier (which led to a massive premium increase), and of course, a devastating conversation with the real seller. The reputational damage within the local real estate community was immediate and severe.

How a Modern Workflow Prevents This Exact Scenario

This loss was not a technology failure; it was a workflow failure. A modern, secure workflow anticipates these attacks and builds a system where this chain of events is impossible. CloseSimple integrates with your TPS to replace these high-risk manual gaps with a secure, auditable platform.

|

The Point of Failure |

The Manual Process That Failed |

The CloseSimple Secure Workflow |

The Claim Prevention Value |

|---|---|---|---|

|

Receiving Instructions |

Accepting wire instructions from an email attachment. |

All sensitive documents must be exchanged within a secure, white-labeled portal. |

Ends email as a potential point for fraud. Trains clients to distrust emailed instructions. |

|

Verifying Changes |

"Confirming" details by replying to the fraudulent email. |

Wire instructions are locked behind a mandatory e-signature acknowledgment. |

Creates a perfect, immutable audit trail. The real client must log in to approve. |

|

Final Check |

Relying solely on the processor to spot a fake before sending. |

Wire Verification automatically matches account details before funds are moved. |

Adds an automated final checkpoint to catch any potential human error. |

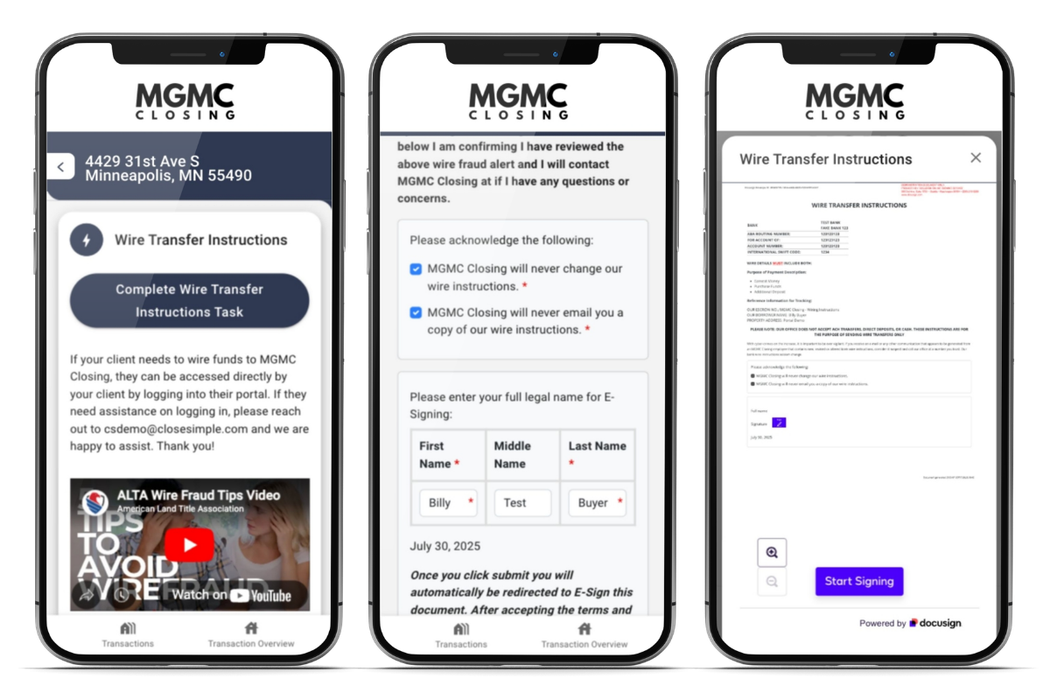

1. Moving All High-Risk Steps into a Secure, Branded Portal

With CloseSimple, wire instructions and payoff details are never sent via email. They are securely hosted in a 100% white-labeled portal. Your client must log into a space they recognize and trust. This single change eliminates the primary vector for wire fraud entirely. If an email with "new instructions" arrives, your client instantly knows it's a scam because it's not in the portal.

2. Creating an Immutable, E-Signed Audit Trail

Before a client can even view wire instructions in the portal, they are required to complete a multi-factor authentication and provide a certified e-signature acknowledging the details. This creates a powerful, non-repudiable record that proves the legitimate party approved the transaction, protecting you from claims and litigation.

.png?width=600&height=400&name=2025%20Working%20Doc.%20Feature%20Images%20for%20Web%20(1).png)

3. Integrating Automated Security Checks

CloseSimple bakes security directly into the workflow your team already uses inside your TPS (SoftPro, ResWare, Settlor).

- Early Scan: Passively analyzes every file for seller impersonation risk from day one.

- Biometric Liveness Checks: For high-risk remote sellers, we confirm identity against thousands of global documents.

- Wire Verification: Before funds are disbursed, the system automatically verifies routing and account details, ensuring funds go to the correct recipient.

This is backed by a team that understands the urgency of title operations.

Every CloseSimple implementation includes a Dedicated Success Manager, comprehensive post-launch training, business day technical support with responses often under two hours, and the peace of mind of SOC 2 Type II Certification.

This Doesn't Have to Be Your Story

This $240,000 loss was preventable. It was the direct result of relying on an outdated, email-centric workflow in an era of sophisticated cybercrime. By building a process that is secure, auditable, and transparent by default, you can ensure this story never becomes your reality.

Ready to see how a modern workflow can protect your company?

Book a CloseSimple Demo Today →

Tags

Wire Instructions

Related posts

Fraud Prevention

What Happens When Wiring Instructions Are Compromised? A Title Company’s Guide

Earnest Money

How Does Earnest Money Fraud Work? Why Don’t Title Companies Catch It Early?

Resources

Why Title Companies Should Route Every Real Estate Closing Payment Through One Portal

Resources

How Tech Prevents Real Estate Wire Fraud | Title Company Security