They say economists have predicted seventeen of the last three recessions. But there’s a chance this could be one of the fourteen. Despite the highest inflation in over forty years, tightening monetary policy, turbulent relations with China, concerns around commercial real estate, and any other issue of the day, the U.S. economy seems stubbornly strong.

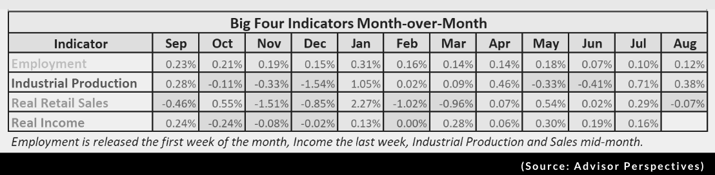

It’s proven to be more resilient than most expected in the face of these multiple headwinds. Let’s get right down to it. Among others, there are four key indicators the Fed relies on—job growth, industrial production, real retail sales and real personal income. The table below shows growth in green or contraction in red. It isn’t exactly sounding the alarm bell lately.

And now you may get the house after two or three offers, part because of rates but also due to historically low inventory. One key difference this time around is that as buyer activity has slowed, so too has seller activity. This has kept the balance of the market persistently tight. During the financial crisis, supply levels rose while demand cratered which almost always results in lower prices.

The trouble, of course, is payments.

The typical payment on the median priced home in the Minneapolis-St. Paul area rose from $1,765 in 2021 to $2,580 per month in 2023. That’s over a forty percent increase in two years or another $9,600 per year in interest. If rates do ease, as they may, buyers will be trading an interest rate problem for a principal problem. List prices will surely increase and multiple offer situations will return, driving prices even higher.

Pick your poison.

And therein lies the rub. Forty two percent of US homes are owned outright. Of the remainder, over two thirds are financed at rates below four percent—think of this as the “golden handcuffs” for would-be sellers. So don’t expect housing supply to surge any time soon, despite the best attempts from builders. Builders are, however, making up a growing share of a shrinking pie. They aren’t wed to an interest rate and have every incentive to move their product. Many home builder stocks reflect this.

The luxury brackets have outperformed lately, as those buyers are less rate sensitive. Townhomes have also been a growth segment as flustered buyers desperately seek budget-friendly monthly payments.

Home prices have never mattered as much as home payments. And ultra-low interest rates protected buyers from feeling the effect of rising prices on their monthly payments. But no more. On the bright side, we’re earning over four percent on savings.

The biggie: what does the future hold?

Nobody knows.

Run away from anyone saying they do. One thing is for sure: we’re in uncharted waters. An election is approaching and geo-political tensions remain elevated alongside other headwinds. The soft landing odds have increased though bond markets are less convinced than equity markets.

As for housing, it’s difficult to imagine a crash without higher levels of delinquency. The best time to buy a home?

When you’re ready. But since rates may moderate to the low-sixes or high-fives, that would reignite bidding wars and accelerate buyer activity. An increase in multifamily development is starting to push rents down.

Many expected recession to appear in the third or fourth quarter of this year but that’s seemingly shifted to mid-2024. The CPI shows inflation slowing from over nine percent to around three percent—ever closer to the Fed’s sweet spot. Even so, a pause in rate hikes is not necessarily a pivot. So hold your horses.

We may not be out of the woods but we don’t seem to be going further in either—at least not at the moment. Then again, there’s a lag between rate hikes and their full effect on, say, commercial real estate among other things. Just remember that a recession does not mean a housing crisis.

The Growth & Scale Report is published by CloseSimple, and explores strategies for growth and tools for scaling your title or escrow company. The report emphasizes the art of balancing growth and scale, with a focus on personal and organizational success stories. It aims to share insights from industry leaders who have navigated these challenges, providing a platform for broader conversations in the business landscape.

Related posts

Resources

Growth & Scale Report: [FULL STORY] Brie McDaniel & Kay Underwood on Connecting the Dots in Title & Escrow

Resources

Growth & Scale Report: [FULL STORY] Rick Diamond on Why Scaling Never Goes Out of Style

Resources

Growth & Scale Report: [FULL STORY] Wayne Stanley - Prepare for Day One of Real Estate Agent's New Reality

Resources

Growth & Scale Report: [FULL STORY] Erica Meyer - Forging Paths